1. What is a Mortgage Investment Corporation (MIC)?

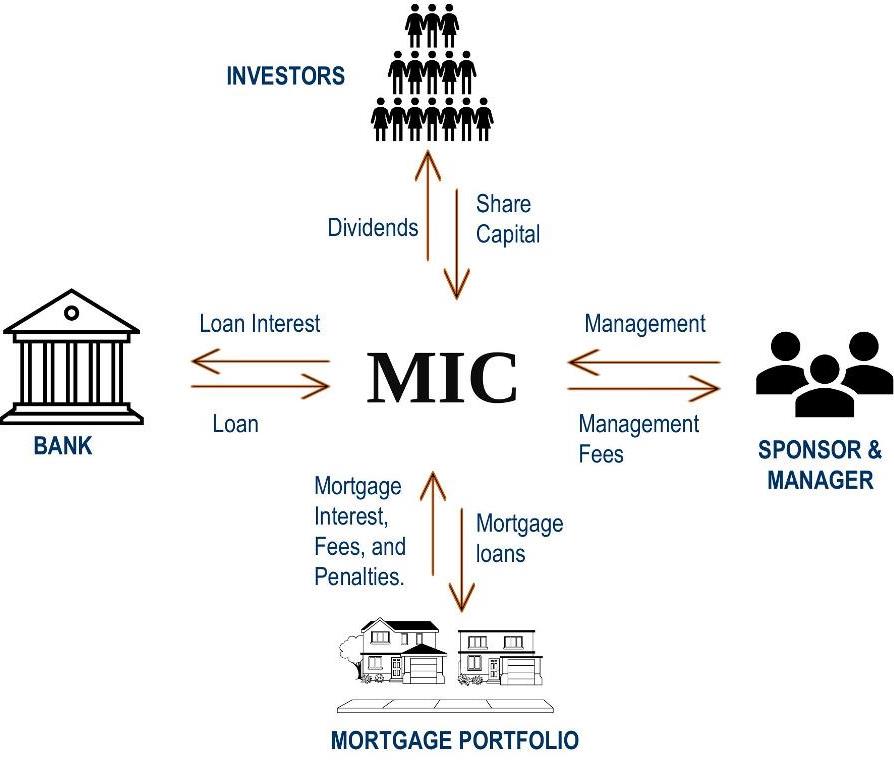

- A Mortgage Investment Corporation or MIC is a special company created by virtue of Section 130.1 of the Income Tax Act, a federal statute put in place in 1973 to enable investors to invest in residential mortgages.

- A Mortgage Investment Corporation (MIC) provides a way to pool funds to invest in residential mortgages thereby mitigating the time and risk of investing in individual mortgages. The pool of mortgages is continuously managed, with newly invested share capital, and the proceeds of repaid and discharged mortgages, being utilized to fund new mortgages.

2. What are the advantages of a MIC structure?

- A MIC is a corporation formed under the rules set out in the Income Tax Act, Section 130.1.,

- A MIC pools shareholder capital and lends in Canadian residential and commercial mortgages,

- The MIC earns income from those mortgages on interest charges and general fees,

- Mortgage Investment Corporations (MICs) are tax exempt – They do not pay income tax,

- MICs are legally mandated to distribute all their earnings to investors,

- MIC dividend distributions are treated as interest income for tax purposes,

- MICs are “qualified investments” for registered plans including RRSPs, RRIFs, RESPs, TFSAs and others.

3. Show me a MIC structure.

4. How does a corporation qualify as a MIC?

To Qualify as a MIC annually for tax purposes, the corporation must meet the guidelines below:

Income Tax Act, Section 130.1: Salient Rules

- A Mortgage Investment Corporation must have at least 20 shareholders.

- A MIC is generally widely held. No shareholder may hold more than 25% of the MIC’s total capital.

- At least 50% of a MIC’s assets must be comprised of residential mortgages, and/or cash and insured deposits at Canada Deposit Insurance Corporation member financial institutions.

- A MIC may invest up to 25% of its assets directly in real estate, but may not develop land or engage in construction. This ceiling on real estate holdings does not include real estate acquired as a result of mortgage default.

- A MIC is a flow-through investment vehicle and distributes 100% of its net income to its shareholders.

- All MIC investments must be in Canada, but a MIC may accept investment capital from outside of Canada.

- A MIC is a tax-exempt corporation.

- Dividends received with respect to directly held shares, not held within TFSA, RRSPs or RRIFs, are taxed as interest income in the shareholder’s hands. Dividends may be received in the form of cash or additional shares.

- MIC shares are qualified TSFA, RRSP and RRIF investments.

- A MIC may distribute income dividends, typically interest from mortgages and revenue from property holdings, as well as capital gain dividends, typically from the disposition of its real estate investments.

- A MIC’s annual financial statements must be audited.

- A MIC may employ financial leverage by using debt to partially fund assets.

5. Who Can Sponsor a MIC?

Individuals, corporations, charitable organizations, Clubs, and Other Groups.

6. What are the Responsibilities of a MIC Sponsor?

The Sponsors are the founders of the MIC, who must do the following:

- Register the Corporation, and Attract a minimum of 20 investors to the MIC,

- Arrange for Exempt Market Dealer and Mortgage Administrator companies.

- Pay for the initial legal cost of MIC offering and subscription documentation, and

- Provide monitoring and reporting to the investors.

7. What are the benefits of promoting / starting a MIC?

- A simple way to start and run a profitable multi-million-dollar fund

- Add value to your membership to grow income and capital

- Boost your operating revenue from fees from managing your MIC

- Take a advantage of group economics of scale

8. Who owns the MIC?

- Mortgage Investment Corporations (MICs) are owned by the investors.

- A MIC must be widely held. No shareholder may hold more than 25% of the MIC’s total capital.

9. How does MIC make money?

- A MIC’s revenues are comprised of mortgage interest and fee income.

10. What are MIC’s Expenses?

A MIC’s Expenses are predominantly comprised of:

- Offering cost – registration, the legal cost for offering memorandum and subscription documentation,

- Management fees, audit and other professional fees, and loan interest, if the MIC is employing debt in addition to share capital.

11. What are the Roles of Exempt Market Dealer and Mortgage Administrator in a MIC?

The EMD and Mortgage Administrator help with:

- Adherence to regulatory compliance requirements

- Administering the mortgages and management of the MIC,

- Sourcing of suitable mortgage investments,

- Analysis of mortgage applications, negotiation of suitable interest rates, terms, and conditions,

- Instruction of solicitors, mortgage portfolio and general administration.

12. What are the benefits of investing in a MIC?

- Secured Investment: Mortgages purchased by the MIC are secured by Canadian Residential Real Estate.

- Safety through Diversification: Investors in MIC own a diversified portfolio of mortgage loans which can reduce risks.

- Capital Preservation Strategy: The MIC investment strategy has a low correlation with traditional assets that can help preserve capital invested, especially given the volatility of the traditional asset class.

- Superior Returns: Earn up to 9% per year compared with 2% on GICs. MIC investments have traditionally outperformed bonds and GICs over the long term.

- Professional Management and Regulatory Oversight: The management of the MIC has oversight from the Ontario Securities Commission (OSC) and Financial Services Regulatory Authority of Ontario (FSRA).

- Regular Dividend Distribution: Investors receive their dividends on quarterly or monthly dividend distribution dates.

- Tax Savings: Mortgage investment funds are RRSP, TFSA and RRIF eligible.

- No Double Taxation: MIC is tax-free so, only the dividend from a MIC is taxed as interest income in the hands of the investors. This is a significant advantage for MIC investors because this increases the yield as the two levels of tax applied to regular corporations and their investors are avoided.

13. Who are the parties involved in a MIC investment?

- Shareholders/Investors: These individuals and corporations are also known as ‘Unit Holders’ or “Investors”. Such investors would subscribe to units in the MIC. Unit holders have the right to receive any form of return from the asset, according to the initial agreement entered by the unit holder and the company.

- Exempt Market Dealer (EMD): The EMD has the sole responsibility of overseeing the capital raising and compliance with the securities’ regulatory requirements of the MIC. The EMD is responsible for making sure of investor suitability, completing the subscription agreement, know your client (KYC) and know your product (KYP) forms.

- Legal Firm: The law firm prepare the initial Offering Memorandum, Subscription Agreement and guide for completing a subscription agreement, the exemption from prospectus certificates and acknowledgements, the know your client (KYC) and know your product (KYP) forms.

- Manager or Sponsor: To safeguard the interests of the investors, a Board of Directors is appointed by the MIC Manager to act for the benefit of the shareholders.

- Mortgage Administrator: The Mortgage Administrator is responsible for managing mortgage investment – receiving mortgage payments from borrowers on behalf of the MIC, monitoring the agreement and taking steps and enforcing mortgage payments. The administrator is responsible for advising the shareholder, valuation of the fund and management of the fund.

- Mortgage Broker: In a MIC the Mortgage Broker is responsible for negotiating the best available terms and rates with lenders. They consider a borrower’s financial history, down payment when necessary and the type of property they are interested in borrowing against and liaison between a borrower and a lender and do much of the paperwork.

- CPA Firms: The Income Tax Act requires that 100% of a MIC’s annual net income be audited by an external CPA firm to ensure the MIC’s net income is distributed to its shareholders, in the form of a dividend.

1. What is a Mutual Fund Trust (MFT)?

A mutual fund trust is a unit trust whose units are all held and circulate in accordance with the prescribed conditions governing:

- the number of units holders;

- the dispersal of ownership of the units; and

- public trading of the units.

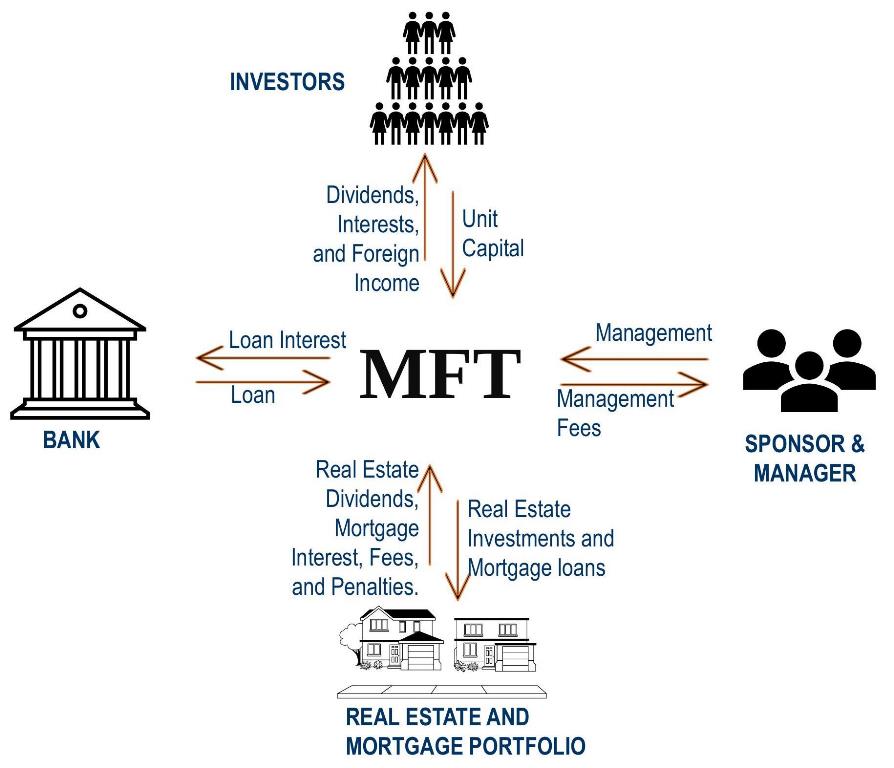

A Mutual fund Trust (MFT) provides a way to pool funds to invest along with other unitholders (investors in the fund) in investing in certain real property, and certain activities relating to real property. The exact mix of the investment depends on the objectives of the fund, with the aim to generate income for the fund, generally in the form of interest or dividends. All of the income received by the fund (net of fund expenses) is paid out to unitholders on a monthly, quarterly or annual basis, as it’s earned.

2. What are the advantages of a MFT structure?

- A Mutual Fund Trust (MFT) is a Trust formed under the rules set out in the Income Tax Act, Section 132

- A MFT pools shareholder capital and invests in real estate related products – mortgages and real estate.

- Units may be “qualified investments” for RRSPs, RRIFs, RESPs, TFSAs and other registered plans

- Exemption from Part XII.2 tax for non-residents of Canada to reduce their tax burdend,

- Capital gains refund mechanism that to limit potential double taxation on capital gains

- Exemption from alternative minimum tax which can trigger unexpected tax liability,

- Exemption from 21 year deemed disposition rule

- The MFT earns income from those real estates and mortgages on capital gains and interest charges and general fees.

- If all income earned by MFT is distributing to its unitholders, it is tax free,

- If the MFT retains earnings, the fund can use the distributed income to Unitholder as benefits to minimizing the overall taxes paid by the fund, since mutual fund trusts are taxed at a rate equivalent to the highest personal tax rate.

- Distributing income to unitholders, most of whom are taxed at a lower marginal tax rate than the mutual fund, generally results in a lower amount of total taxes paid.

- By reducing tax paid by the fund, more income can be distributed to investors, which improves the return on their investment.

3. Show me a MFT structure.

4. How does an entity qualify as an MFT?

To qualify as a “mutual fund trust (MFT)”, a trust must generally satisfy the following conditions on an ongoing basis:

- The trust must be resident in Canada for the purposes of the Tax Act;

- The trust must be a “unit trust” for the purposes of the Tax Act;

- To qualify as a “unit trust”, the trust must generally pass one of the following tests:

- at least 95% of the units of the trust (based on their fair market value) have conditions attached to them requiring the trust to accept, at the demand of the unitholder and at prices determined and payable in accordance with the conditions, the surrender of the units (the “Redeemable on Demand Condition”), or

- the assets, activities and income of the trust satisfy a prescribed set of character and dispersal requirements.

- The trust must restrict its undertakings to:

- the investing of its funds in certain property, and

- certain activities relating to real property; and

- The trust must satisfy certain prescribed conditions, including the requirement that 150 separate unitholders each hold, in respect of a single qualifying class of units, not less than one “block of units”1 of the class having an aggregate fair market value of at least $500 (the “150 Unitholder Condition”).

5. Who Can Sponsor an MFT?

Individuals, corporations, charitable organizations, Clubs, and Other Groups.

6. What are the Responsibilities of a MFT Sponsor?

The Sponsors are the founders of the MFT, who must do the following:

- Issue the Declaration of Trust, Operating Trust, offering documentation, and Attract a minimum of 150 investors to the MFT,

- Arrange for Exempt Market Dealer and Mortgage Administrator companies.

- Pay for the initial legal cost of MFT offering and subscription documentation, and

- Provide monitoring and reporting to the investors.

7. What are the benefits of promoting / starting an MFT?

- A simple way to start and run a profitable multi-million-dollar fund

- Add value to your membership to grow income and capital

- Boost your operating revenue from fees from managing your MIC

- Take a advantage of group economics of scale

8. Who owns the MFT?

- Mortgage Investment Corporations (MICs) are owned by the investors.

- MFT must be widely held by a minimum of 150 unitholders and there is no restriction on numbers of units that can be held by an individual or family.

9. How does MFT make money?

MFT’s revenues are comprised of dividend and mortgage interest and fee income.

10. What are MTF’s Expenses?

MFT’s Expenses are predominantly comprised of:

- Offering cost – registration, the legal cost for offering memorandum and subscription documentation,

- Management fees, audit and other professional fees, and loan interest, if the MFT is employing debt in addition to share capital.

11. What are the Roles of Exempt Market Dealer and Mortgage Administrator in an MFT?

The EMD and Mortgage Administrator help with:

- Adherence to regulatory compliance requirements

- Administering the mortgages and management of the MFT,

- Sourcing of suitable mortgage investments,

- Analysis of mortgage applications, negotiation of suitable interest rates, terms, and conditions,

- Instruction of solicitors, mortgage portfolio and general administration.

12. What are the benefits of investing in a MFT?

- Secured Investment: Mortgages purchased by the MFT are secured by Canadian Residential Real Estate.

- Safety through Diversification: Investors in MFT own a diversified portfolio of real estate and mortgage loans which can reduce risks.

- Capital Preservation Strategy: The MFT investment strategy has a low correlation with traditional assets that can help preserve capital invested, especially given the volatility of the traditional asset class.

- Superior Returns: Earn up to 9% per year compared with 2% on GICs. MFT investments have traditionally outperformed bonds and GICs over the long term.

- Professional Management and Regulatory Oversight: The management of the MFT has oversight from the Ontario Securities Commission (OSC) and Financial Services Regulatory Authority of Ontario (FSRA).

- Regular Dividend Distribution: Investors receive their dividends on quarterly or monthly dividend distribution dates.

- Tax Savings: Mortgage investment funds are RRSP, TFSA and RRIF eligible.

- No Double Taxation: MFT is tax-free if all dividends are distributed, only the distribution from an MFT is taxed as interest income in the hands of the investors. This is a significant advantage for MFT investors because this increases the yield as the two levels of tax applied to regular corporations and their investors are avoided.

13. Who are the parties involved in a MFT investment?

- Unitholders: These individuals and corporations are also known as ‘Unit Holders’ or “Investors”. Such investors would subscribe to units in the MFT. Unit holders have the right to receive any form of return from the asset, according to the initial agreement entered by the unit holder and the company.

- Exempt Market Dealer (EMD): The EMD has the sole responsibility of overseeing the capital raising and compliance with the securities’ regulatory requirements of the MFT. The EMD is responsible for making sure of investor suitability, completing the subscription agreement, know your client (KYC) and know your product (KYP) forms.

- Legal Firm: The law firm prepare the initial Declaration of Trust, Operating Trust, Offering Memorandum, Subscription Agreement and guide for completing a subscription agreement, the exemption from prospectus certificates and acknowledgements, the know your client (KYC) and know your product (KYP) forms.

- Manager or Sponsor: To safeguard the interests of the investors, a Board of Trustee is appointed by the MFT Manager to act for the benefit of the shareholders.

- Mortgage Administrator: The Mortgage Administrator is responsible for managing mortgage investment – receiving mortgage payments from borrowers on behalf of the MFT, monitoring the agreement and taking steps and enforcing mortgage payments. The administrator is responsible for advising the shareholder, valuation of the fund and management of the fund.

- Mortgage Broker: In a MFT the Mortgage Broker is responsible for negotiating the best available terms and rates with lenders. They take into account a borrower’s financial history, down payment when necessary and the type of property they are interested in borrowing against and liaison between a borrower and a lender and do much of the paperwork.

- CPA Firms: The Income Tax Act requires that 100% of a MFT’s annual net income be audited by an external CPA firm to ensure the MFT’s net income is distributed to its shareholders, in the form of a dividend.